Republic Act No. 11524, or the Coconut Farmers and Industry Trust Fund Act, took effect on March 13, 2021.

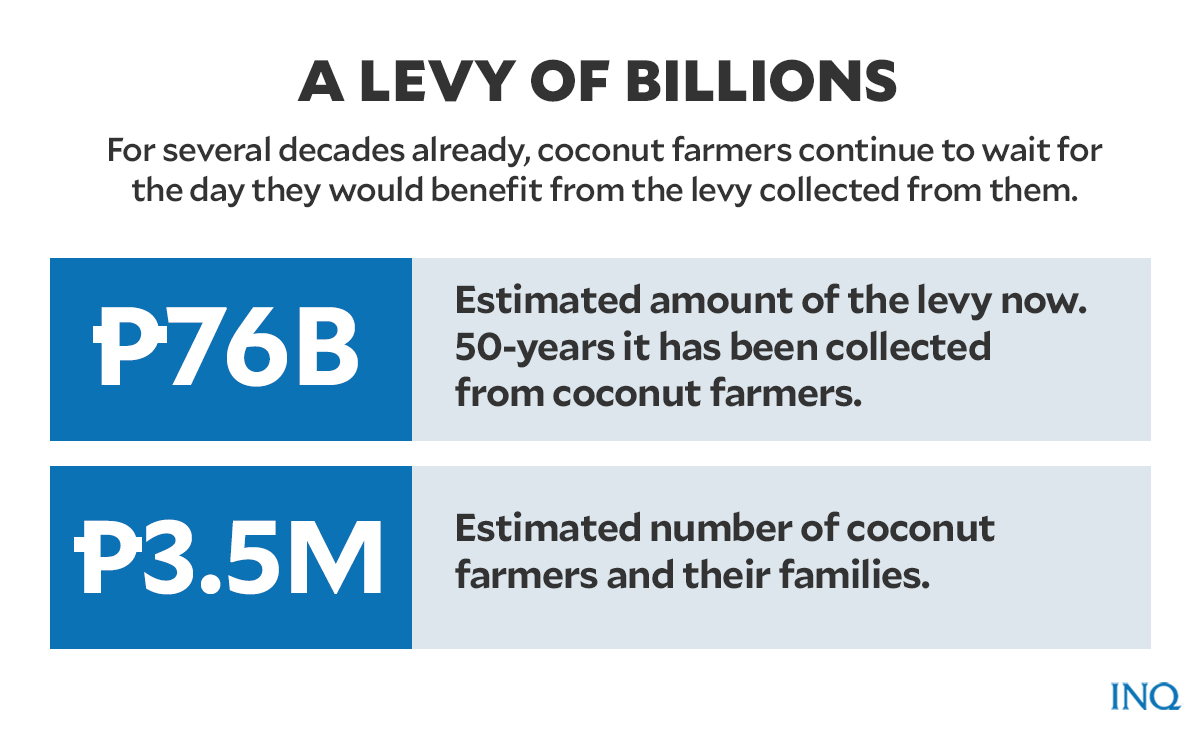

To manage the consolidated coconut levy collections currently worth at least P76 billion, the law created the Trust Fund Management Committee (TFMC), composed of the Departments of Finance (DOF), Budget and Management (DBM) and Justice (DOJ).

The TFMC is tasked with drafting the implementing rules and regulations (IRR) governing management of the consolidated coconut trust fund. While RA 11524 is silent on who approves the proposed rules, the three agencies appear bent on passing their own draft through a joint memorandum-circular.

But critical questions need to be raised:

- Why allot only one week for submission of stakeholders’ comments? Why the undue haste in issuing the IRR? The Supreme Court has ruled that the trust fund is a “public fund held in trust by the government for the exclusive benefit of the coconut farmers and the industry”.

- For the fund that will finance economic and social programs for desperately poor coconut farmers, will genuine public hearings and consultations on its proper administration be held?

- How will the Executive satisfy the demand for public transparency and protecting the interests of the fund’s beneficial owners—the country’s 3.5 million coconut farmers and farm workers?

Although hugely disappointed and angered by the law’s serious deficiencies, the organized coconut peasantry stands ready to contribute proposals to secure maximum benefits for farmers long struggling to recover their forced levy contributions these past 50 years.

During congressional deliberations on RA 11524, its principal authors contended that coconut farmers lacked the financial expertise to participate in the management of the fund. Thus, Congress left the fund entirely in the hands of the Executive, particularly the DOF which was designated as fund manager. The repercussions of excluding farmers can be seen in the TFMC’s inability to address the concerns and interests of farmers in the draft IRR.

In this regard, we cite the TFMC’s major omissions and overreach in its draft:

-

No report on interest earnings since 2015.

The P69.5 billion in proceeds from the sale of San Miguel Corporation (SMC) preferred shares had appreciated to P76 billion, when turned over to the Special Account in the General Fund (SAGF) of the Bureau of Treasury (BTr) in 2015. This was after the Supreme Court had ordered the funds’ transfer from the levy-sourced Coconut Industry Investment Fund (CIIF). From 2015 to the present, no accounting of interest earned by the SAGF has been made to coconut producers.

The DOF claims that the P76 billion had been frozen, or cannot be invested and is non-interest bearing, since 2015 citing a Supreme Court ruling that a new law was needed to utilize the fund.

Yet, despite the enactment of RA 11524, the amount could not be remitted entirely to the trust fund account in the Treasury. Legislators simply continued the free use of the money via a provision allowing government to return the full amount within five years.

Additionally, RA 11524 provides for interest on the fund in the fifth year, but is silent on the application of interest in prior years. The IRR should put clarity to this.

Further, the mere fact that the lump sum could not be transferred from the SAGF would mean that the P76 billion intended for the trust fund have been invested and thus, earning interest since 2015. Rightfully, all these should be accounted for and returned to the fund for the benefit of coconut farmers.

-

Opaque disposition of non-cash assets (United Coconut Planters Bank and CIIF Oil Mills)

RA 11524 provides only for proceeds from privatization of coconut levy assets within five years to flow back to the trust fund. It does not specify how these assets may be used in their current state to better serve the coconut farmers and industry.

On the other hand, government—especially DOF—had been aggressively pushing for UCPB’s merger with, or purchase by, the Land Bank of the Philippines (LBP) even before RA 11524 took effect and its IRR approved!

The fates of UCPB and the CIIF Oil Mills are definitely of great concern to the coconut sector.

The Presidential Commission on Good Government (PCGG) reported the total worth of shares in these companies at P30-P40 billion. Their value, however, may be compromised due to an apparent design to undermine the process of their disposition. This will likely shortchange the coconut farmers by the billions.

As the fund’s beneficial owners, farmers deserve the fullest protection of their interests in the disposition of the fund’s non-cash assets. This is not guaranteed if they have no participation in the valuation, vetting of buyers, and other key areas in asset disposition.

-

Absence of consultative mechanism with coconut farmers

The partially recovered coconut levies (there are more assets disputed in court) form the initial capitalization of the trust fund.

Without transparency, however, government cannot just demand complete trust by virtue of being the fund holder. RA 11524 being sorely quiet on the matter, the IRR can give enlightenment to the law’s avowed purpose by establishing consultative mechanisms. Trust after all is earned, not commanded.

The lack of dialogue merely engenders speculation about dubious intentions surrounding billions worth of levy funds.

There is much merit in creating a consultative group composed of coconut farmers’ representatives, who will inform the TFMC about their needs, review reports submitted to or by the TFMC, and share inputs on fund management.

-

Reconveyance of disputed coconut levy assets

Disputed levy assets (cash and non-cash) are not subject to reconveyance under RA 11524. The purpose, therefore, of including them in the IRR should be explained.

How will the IRR protect coconut farmers in negotiations regarding these disputed assets?

With DOF’s primary mandate being revenue generation, how will appraisal of asset dispositions be handled when its revenue maximization objective may not jibe with the interests of coconut farmers or the principal government agency mandated to serve the needs of farmers and coco-based industries?

-

Budget for Trust Fund Management expenses

Section 10 of RA 11524 allocates 0.5 percent of the trust fund principal in a given year for TFMC expenses. This sum is estimated to run to hundreds of millions. But which principal is referred to? The entire amount of cash and assets, even when not yet transferred to the trust fund, including interests?

The fund management fee may be excessive. Ordinarily, fund managers are rated in terms of projected returns earned by the fund.

Fund management fee must be a reasonable portion of fund earnings.

RA 11524 limits trust fund investments to “Philippine government securities and other securities guaranteed by the national government”.

Hence, actual fund management will not be complicated, although related work, like managing and investing “non-cash coconut levy assets” could be, depending on what these are. The management fee must be treated not as a fixed amount but as the ceiling for expenditures, which should be matched against the level of earnings generated by a fund manager.

An Appeal

Positive action on these vital concerns will safeguard our coconut farmers, already impoverished by the coco levy during martial law, from being scammed twice—depriving the trust fund of interest earnings since 2015 and compromising fund recovery through opaque privatization schemes—and thrice if the funds were depleted through excessive management fees.

(Editor’s note: Leonardo Q. Montemayor is chair of the Federation of Free Farmers and former agriculture secretary. Charles R. Avila is executive director of Confederation of Coconut Farmers’ Organization of the Philippines and former Philippine Coconut Authority administrator. Joey T. Faustino is adviser of the Coconut Industry Reform Movement)